Introduction

Most insurance companies that deployed chatbots over the last few years believe they've checked the "AI automation" box. They point to FAQ deflection rates, appointment scheduling bots, and premium reminder systems as evidence of digital transformation. But there's a widening chasm between what these rule-based chatbots deliver and what modern AI agents can actually accomplish in insurance operations.

The gap hits harder in insurance than in most other industries. Unlike a retail return or a password reset, insurance interactions are rarely simple:

- Complex policy language with variable coverage terms

- Multi-step claims requiring coordination across adjusters and third parties

- Strict regulatory compliance with audit trail requirements

- Customers reaching out during high-stress moments — post-accident, mid-hospitalization, post-disaster

When a chatbot fails at these touchpoints, it doesn't just frustrate customers. It damages trust, triggers regulatory complaints, and drives 83% of consumers to consider switching carriers.

Traditional chatbots were built to answer questions. AI agents are built to resolve interactions — and in insurance, that difference in scope determines whether automation actually reduces costs or quietly creates new ones.

TL;DR

- Traditional chatbots follow scripts; AI agents understand intent, handle context, and complete multi-step tasks end-to-end

- In insurance, real customer interactions—claims, policy changes, billing disputes—require actions, not just answers

- AI agents connect to core systems and execute workflows; chatbots mostly retrieve information

- The real gap is whether your automation resolves interactions or just deflects them

- Insurers treating AI agents as "better chatbots" miss the scale of the shift—and the efficiency gains that come with it

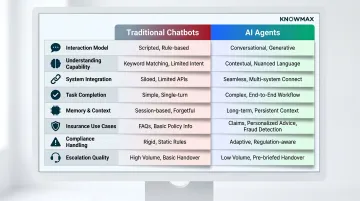

Traditional Chatbots vs. AI Agents in Insurance: Quick Comparison

| Dimension | Traditional Chatbots | AI Agents |

|---|---|---|

| Interaction Model | Script-driven, reactive prompts | Goal-oriented, multi-step execution |

| Understanding Capability | Keyword matching, shallow NLU | Contextual intent recognition via LLMs |

| System Integration | Read-only API connections | Bi-directional execution (read + write) |

| Task Completion | Retrieve information, link to forms | Initiate claims, execute policy changes |

| Memory & Context | Session-only, no cross-channel memory | Unified view across sessions and channels |

| Insurance-Specific Use Cases | FAQs, premium reminders, basic triage | FNOL automation, endorsements, billing actions |

| Compliance Handling | Manual script updates, high lag risk | Governed knowledge base, audit trails |

| Escalation Quality | Blind transfers, no context passed | Context-rich handoffs with transcript and next action |

Traditional chatbots remain appropriate for narrow, high-volume tasks—premium due reminders, office hours inquiries, document checklists. Claims intake, policy changes, and billing disputes demand judgment and system access that script-driven bots simply cannot provide.

What Are Traditional Chatbots — And Why Do They Fall Short in Insurance?

Traditional chatbots are rule-based, script-driven systems that operate on decision trees and keyword recognition. Even AI-enhanced chatbots using natural language understanding remain fundamentally reactive—they respond to prompts but cannot initiate actions or deviate meaningfully from programmed paths.

Chatbots work off predefined dialogue flows and shallow API connections that let them read limited data — but not act on it. In insurance, this distinction matters. A chatbot can confirm a policy number exists but cannot initiate a claim, process an endorsement, or explain a partial claim rejection using actual policy context. It retrieves information; it doesn't execute workflows.

The Script Boundary Problem

The most damaging limitation in insurance is the "script boundary" problem. The moment a customer asks something outside the decision tree—"Why was my claim only partially approved?" or "Can I backdate this coverage?"—the chatbot either gives a generic response or escalates to a human. Industry research shows that 31% of chatbot conversations require human escalation, and qualitative evidence from insurers suggests that figure is higher in insurance due to interaction complexity. Worse, 54% of consumers say they would rather wait for a human agent than deal with a bot.

This creates a frustrating cycle: customers attempt self-service, hit the script boundary, escalate to an agent who lacks context from the chatbot session, and the entire interaction starts over. The chatbot didn't resolve anything—it deflected, and often poorly.

Maintenance Burden and Compliance Risk

Insurance products change constantly. In 2024 alone, carriers managed over 3,300 regulatory updates across state and federal levels. Each update potentially requires chatbot script review and revision. This creates a dangerous lag: while compliance teams work through script updates, chatbots continue sharing outdated or inaccurate information with customers—a direct liability in a regulated industry.

Manual script maintenance doesn't scale. Every week a script goes unupdated is a week customers receive answers that may no longer be accurate — or legal.

Use Cases of Traditional Chatbots in Insurance

Traditional chatbots still add value in a few narrow scenarios:

- Sending premium due date reminders and renewal nudges at scale, with no judgment required

- Answering basic FAQs: office hours, document checklists, branch locations, simple definitions

- Collecting contact details and routing customers before human handoff

These work because the inputs are predictable and the outputs are fixed. The moment a customer needs context-sensitive answers or any backend action, the model breaks down.

What Are AI Agents — And How Are They Reshaping Insurance Operations?

AI agents are goal-oriented systems that use large language models, contextual memory, and bi-directional system integrations to understand intent, plan multi-step actions, and execute tasks. They go well beyond responding to prompts. Unlike chatbots, they can carry conversations across sessions, access live policy and claims data, and trigger real changes in backend systems.

The key differentiator for insurance: AI agents operate as an execution layer, not just an information layer.

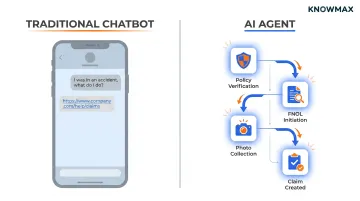

Consider this scenario. A customer says, "I had an accident yesterday, what do I do?" A chatbot provides a link to a claims form. An AI agent verifies the policy, checks coverage limits, initiates First Notice of Loss, collects photos, and creates the claim record—all in the same conversation.

Context Memory and Omnichannel Continuity

Insurance journeys are multi-touchpoint: a customer calls for FNOL, sends documents via WhatsApp, and checks status through a web portal. AI agents maintain a unified view of the customer's case across channels, so policyholders never repeat themselves. Chatbots, by contrast, have no cross-session or cross-channel memory—each interaction starts from scratch.

The Role of Knowledge Foundation

AI agents are only as accurate as the knowledge they're grounded in. A structured, always-updated knowledge layer — covering decision trees, guided resolution flows, and policy documentation — is what separates compliant, accurate responses from generic or hallucinated ones. Platforms like Knowmax provide exactly this foundation, ensuring AI agents surface the right answer for the right insurance context. Without it, even the most capable agent risks delivering outdated information when it matters most.

Use Cases of AI Agents in Insurance

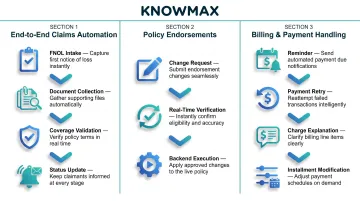

Three high-impact insurance workflows where AI agents outperform chatbots:

1. End-to-end claims automation – from FNOL intake and document collection to coverage validation and status updates. Leading insurers using AI agents achieve 45% faster claim registration and significant drops in incomplete submissions.

2. Policy endorsements – adding drivers, changing nominees, updating addresses with real-time verification and backend execution. The agent handles the change directly, not just the explanation of how to request one.

3. Billing and payment handling – overdue reminders, payment retries, charge explanations, installment modifications. Rather than directing customers to a payment portal, the agent processes the transaction within the same conversation.

Beyond these core workflows, two emerging use cases are gaining traction:

- Proactive service – AI agents that warn policyholders before policies lapse, flag missing claim documents, or detect FNOL inconsistencies before they delay processing

- Intelligent escalation – detecting customer frustration or complexity signals and escalating to human agents with full context, transcript, and recommended next action, rather than a blind handoff

For insurance specifically, AI agents can be configured to maintain audit trails, verify identity securely, and operate within regulatory guardrails — making compliance a built-in feature, not an afterthought.

Why the Capability Gap Is Bigger in Insurance Than You Think

Insurance interactions are fundamentally different from retail or telecom support. A customer asking about their phone bill has a simple transaction at stake. A customer filing a total-loss auto claim or disputing a health claim denial is navigating financial stress, legal implications, and complex policy language. The bar for "helpful" is dramatically higher in insurance—and chatbots simply cannot clear it.

The Complexity Multiplier

Insurance carries a unique complexity multiplier:

- Policy language varies across types, riders, and exclusions — coverage for the same incident can differ significantly

- Claims require coordinating customers, adjusters, third-party vendors, and repair shops across misaligned timelines

- Regulatory compliance demands accurate disclosures, audit trails, and data handling that generic chatbot scripts cannot guarantee

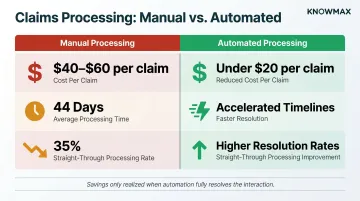

Only 35% of claims achieve straight-through processing industry-wide, and average processing times exceed 44 days while 82% of customers expect payouts within five days. That gap is where automation must deliver—and chatbots don't.

Trust and Emotional Stakes

Insurance customers are often contacting support at their most stressed moments: post-accident, after a medical emergency, during a natural disaster. Chatbots that loop, fail to understand context, or provide generic responses at these moments don't just lose a ticket—they damage brand trust and potentially trigger regulatory complaints.

60% of insurance customers would switch providers for more personalized service, not after a rate increase or claims dispute, but simply because another carrier treated them as an individual. Chatbots respond to inputs. AI agents respond to people — with context, policy history, and the ability to adapt mid-conversation.

Hidden Operational Cost of Chatbot Limitations

Every failed chatbot interaction that escalates to a human agent carries the full cost of agent time plus longer handle time due to lack of context. The chatbot didn't reduce costs—it added friction.

Manual claim processing costs $40–$60 per claim; with automation, costs drop below $20. Those savings only appear when automation actually resolves the interaction. A chatbot that deflects to a human agent delivers zero savings — and often increases cost through repeat contacts.

Compliance and Knowledge Decay Risk

A chatbot with stale scripts is not just unhelpful—it is a liability. Statements generated by AI chatbots are legally treated as direct representations of the company, and inaccurate or unsubstantiated statements can trigger enforcement under federal and state Unfair or Deceptive Acts or Practices statutes.

AI agents backed by a dynamic knowledge management system like Knowmax stay current and auditable across every interaction. When regulatory changes occur, updates propagate instantly to agent desktops, self-service portals, and AI agent workflows — so outdated scripts never reach a customer.

Which One Does Your Insurance Operation Actually Need?

Insurers in early automation stages can start with chatbots for high-volume, low-complexity tasks—FAQ deflection, renewal reminders—but treat them as a bridge, not a destination. Once you're processing claims, handling policy changes, or managing multi-step customer journeys at scale, chatbots run out of road. That's when AI agents become the operational requirement.

Readiness Signals

Signs that an insurer has outgrown their chatbot:

- High escalation rates (approaching or exceeding 30%)

- Frequent "I couldn't understand that" responses in transcripts

- Agents spending significant time re-explaining information the bot already captured

- Customer complaints about having to repeat themselves across channels

- Compliance teams flagging outdated or inaccurate chatbot responses

The Transition Path

If those signals sound familiar, the answer isn't a full system replacement overnight. Start with the highest-friction workflows—claims FNOL, policy changes—get the knowledge foundation solid and structured, then expand from there.

That knowledge foundation is where the transition either holds or breaks down. AI agents need a reliable, compliant, and continuously maintained knowledge base to function accurately. Without one, even a well-configured AI agent will produce hallucinated answers or pull from outdated policy information—both serious risks in insurance. Knowmax's guided decision trees and AI-powered knowledge delivery give insurance contact centers the structured backbone that makes this transition work.

See how Knowmax helps insurance teams build the knowledge foundation AI agents need to fully resolve interactions, not just respond to them.

Conclusion

Traditional chatbots and AI agents don't just differ in capability — they operate on fundamentally different logic. One retrieves; the other reasons and acts. In insurance, where every interaction carries policy complexity, financial stakes, and regulatory weight, that difference determines whether automation actually resolves customer problems or simply delays them.

The real challenge now is the foundation those agents run on. AI agents are only as effective as the knowledge they draw from — which means accuracy, compliance, and continuous updates aren't optional. For insurance organisations investing in agentic automation, getting the knowledge infrastructure right is what separates genuine resolution from a more sophisticated dead end.

Frequently Asked Questions

Frequently Asked Questions

What is the difference between AI agents and traditional chatbots?

Traditional chatbots follow pre-programmed scripts and can only retrieve information based on keyword matching or decision trees. AI agents use large language models and contextual reasoning to understand intent, connect to live systems, and complete multi-step tasks. Traditional chatbots follow pre-programmed scripts and can only retrieve information based on keyword matching or decision trees. AI agents use large language models and contextual reasoning to understand intent, connect to live systems, and complete multi-step tasks. That distinction makes them capable of resolving interactions rather than just responding to them.

What is the most practical application of AI in the insurance industry?

Claims automation, from FNOL to resolution, is the highest-impact use case: it cuts processing time, improves accuracy, and raises customer satisfaction scores. Policy endorsements and proactive renewal management follow closely, since these workflows require AI agents to execute actions, not just surface information.

Can insurance companies use both chatbots and AI agents at the same time?

Yes, a tiered approach is common—chatbots handle simple, high-volume tasks like FAQs and reminders, while AI agents take over complex, action-required workflows. The key is ensuring seamless handoffs and a unified knowledge layer so customers experience consistency across both.

Yes, a tiered approach is common. Chatbots handle simple, high-volume tasks like FAQs and reminders, while AI agents take over complex, action-required workflows. The key is ensuring seamless handoffs and a unified knowledge layer so customers experience consistency across both.

How do AI agents handle compliance and regulatory requirements in insurance?

AI agents can be configured with compliance guardrails, maintain full audit trails, handle secure identity verification, and pull from a governed knowledge base. That combination directly reduces the risk of inaccurate disclosures, which is a real liability with unmanaged chatbot scripts.

What insurance workflows are best suited for AI agents vs. traditional chatbots?

AI agents are best for claims processing, policy changes, billing disputes, and any multi-step workflow requiring backend execution. Traditional chatbots remain adequate only for the narrowest tasks—premium reminders, static FAQ deflection, and initial call triage.