Introduction

Insurance carriers are absorbing pressure from every direction: $137 billion in annual insured catastrophe losses, customers who expect digital-first experiences, and regulatory demands that keep expanding. Traditional automation — rules-based workflows, RPA, scripted chatbots — has reached its ceiling.

40% of underwriter time is still consumed by administrative tasks. Combined ratios are climbing toward 99%, squeezing underwriting margins to near break-even.

Agentic AI changes that equation. Where conventional AI assists — flagging anomalies, drafting content, surfacing recommendations — agentic AI operates autonomously. It perceives inputs, reasons through options, executes tasks, and refines its own behavior based on outcomes. It owns entire workflows, not just individual steps.

This article covers what agentic AI means in an insurance context, the highest-impact use cases across underwriting, claims, fraud detection, and customer service, and what it takes to deploy it successfully.

TLDR:

- Agentic AI owns complete workflows from intake to resolution, not just individual steps

- Insurance's data-rich, process-heavy, high-volume operations are ideal for agentic AI deployment

- Top use cases: claims automation, underwriting acceleration, fraud prevention, and multi-step policy servicing

- Successful adoption requires data governance, regulatory compliance, and workforce upskilling

- Early adopters report 15-45% accuracy gains and 3-5 percentage point loss ratio improvements

What Is Agentic AI in Insurance?

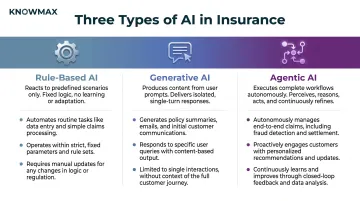

Agentic AI refers to autonomous, goal-driven systems that perceive inputs, reason through options, make decisions, and execute tasks with minimal human instruction. Three types of AI are often confused here:

- Rule-based AI reacts to predefined scenarios with fixed logic

- Generative AI produces content in response to prompts

- Agentic AI takes action across complete workflows, not just isolated steps

In an insurance context, agentic AI collects data from policy administration systems, CRMs, broker submissions, and external sources such as weather databases or property records. It interprets a goal — say, "process this claim" or "underwrite this submission" — then orchestrates the tools, sub-agents, and workflows needed to complete it.

Human oversight is reserved for exceptions or high-stakes decisions. Routine cases flow through autonomously, within regulatory guardrails.

Agentic AI doesn't replace existing infrastructure. It functions as an orchestration layer connecting legacy policy systems, CRMs, data warehouses, and communication channels — adding autonomous decision-making on top of what's already in place.

Why Insurance Operations Are Ripe for Agentic AI

Insurance faces operational pain points that agentic AI is uniquely suited to address:

- Manual underwriting data entry: Underwriters spend 40% of their time on non-core administrative tasks, costing the industry an estimated $17–32 billion annually

- Multi-day claims cycles: Average property claims take 23.9 days to resolve; catastrophe claims average 34.2 days

- Fragmented customer records: Data scattered across systems slows decisions and increases error rates

- High contact center handle times: Repetitive queries consume agent capacity that could be directed toward complex cases

- Compliance documentation burden: Manual logging and audit trail creation divert resources from core operations

The cost of these gaps compounds quickly. $170 billion in global insurance premiums are at risk over five years due to poor claims experiences alone. Slow settlement, inconsistent communication, and lack of transparency drive 80% of dissatisfied customers to switch carriers.

Insurance is data-rich, process-heavy, high-volume, and governed by strict rules. Those are exactly the conditions where autonomous agents perform best. Policies, claims, and underwriting decisions follow repeatable structures, backed by vast historical datasets — giving agentic AI the patterns, rules, and exception data it needs to operate reliably at scale.

The investment numbers reflect that recognition. U.S. insurance technology spending is projected to reach $173 billion in 2026, up 7.8% year-over-year, with industry AI spend as a share of revenue set to triple. Yet only 38% of P&C insurers currently generate value at scale from AI in core workflows — which means the window for first-mover advantage is still open.

Key Use Cases of Agentic AI in Insurance

Agentic AI spans the full insurance value chain. Its value compounds when applied across interconnected processes rather than in isolation.

Underwriting and Risk Assessment

Agentic AI autonomously extracts and validates data from broker submissions, ACORD forms, and third-party datasets such as credit reports or property inspections. It triages applications by risk profile and complexity, routes straightforward submissions for auto-quoting, and flags missing information back to brokers— with no underwriter intervention required on routine cases.

Business impact:

AI has cut standard underwriting decision time from 3-5 days to 12.4 minutes while maintaining 99.3% accuracy. Across carriers, the downstream impact is measurable:

- Complex policy processing time down 31%

- Risk assessment accuracy up 43%

- Loss ratios improved by 3-5 percentage points

- Expense ratios improved by 1-3 percentage points

- Time-to-quote reduced 30-40% among early adopters

Claims Processing and FNOL Automation

Automated first notice of loss (FNOL) across voice, chat, and web channels immediately launches the claim lifecycle. Computer vision models assess damage from submitted photos; AI agents verify policy coverage, coordinate adjusters and repair vendors, and close straightforward claims end-to-end. Complex cases are escalated with full context already assembled.

Business impact:

Faster, more transparent claims resolution drives measurable retention gains:

- Customers with positive claims journeys score 119 NPS points higher than those with negative ones

- Claims promoters are 2.3x more likely to renew — and 3x more likely to renew even after premium increases

Scale matters too. Two Florida hurricanes in 2024 generated over 400,000 claims. Insurers using AI automation reduced FNOL processing time by 8x, absorbing catastrophe surges without proportional staffing increases.

Fraud Detection and Prevention

Agentic AI continuously scans claims submissions, documents, and behavioral patterns across systems to identify anomalies in real time. It compares against historical fraud profiles, flags suspicious activity, blocks payouts where warranted, and autonomously escalates for human investigation. Detection also starts at the application stage, intercepting fraud before policies are ever issued.

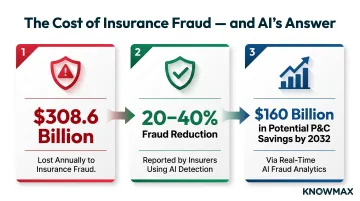

Annual cost of insurance fraud:

The U.S. economy loses an estimated $308.6 billion annually to insurance fraud across all lines. Insurers using AI-driven detection report fraud reductions of 20-40%. Deloitte estimates P&C insurers could save up to $160 billion by 2032 through real-time AI fraud analytics.

Customer Service and Policy Servicing

Basic chatbots handle static queries. Agentic AI goes further — managing policy coverage questions, mid-term changes, renewal conversations, billing disputes, and complaint resolution across digital and voice channels, without human escalation for routine cases.

For this to work at scale, agentic AI needs a reliable, structured knowledge foundation — one that ensures every response is accurate, compliant, and up to date. Knowmax provides that layer for insurance contact centers, combining AI-powered search, guided resolution workflows, and omnichannel delivery into a single platform.

In practice, Knowmax enables insurance teams to:

- Convert complex SOPs into step-by-step guided workflows that agents and AI can follow consistently

- Surface policy and compliance knowledge instantly across agent desktop, self-service portal, chatbot, and mobile

- Use intent-based AI search — not keyword matching — to navigate complex policy language accurately

- Push relevant knowledge into live interactions via CRM integrations with Salesforce, Zendesk, and Genesys

- Maintain audit-ready content with version control and authorization workflows aligned with GDPR, HIPAA, SOC 2, and ISO 27001

Insurance deployments of Knowmax report a 40% reduction in claims and service errors, 80% faster access to policy and compliance knowledge, and a 60% increase in digital self-service adoption.

Regulatory Compliance Monitoring

AI agents automatically log key underwriting and claims decisions, flag activities that deviate from regulatory standards, generate audit-ready compliance reports, and adapt monitoring rules as regulations evolve, removing the manual burden of compliance tracking from operations teams.

Any agentic AI deployment in insurance must itself meet baseline compliance certifications (GDPR, HIPAA, SOC 2, ISO 27001). These are baseline prerequisites, not afterthoughts.

How Agentic AI Transforms Insurance Operations

Operational Efficiency

Agentic AI reduces average handle times in contact centers and claims departments, accelerates quote-to-bind cycles, and eliminates manual data re-entering between systems. According to Accenture research, underwriters spend 40% of their time on administrative tasks versus value-added risk judgment — AI reclaims this capacity for complex decision-making.

Improved Customer Experience

Proactive policyholder communication—storm risk alerts, renewal nudges, personalized coverage recommendations—shifts insurance from a reactive industry to a proactive one. 24/7 resolution capability, without sacrificing accuracy or compliance, meets customer expectations shaped by digital-first experiences.

One carrier using AI generates approximately 50,000 claims-related communications daily. Another implementing intelligent automation for quotes saw 80% of transactions move online, with customer satisfaction rising 36 percentage points.

Cost Reduction and Scalability

Agentic AI enables insurers to handle volume spikes—catastrophe events triggering claims surges, seasonal underwriting peaks—without proportional headcount increases. The financial case is well-documented:

- Forrester predicts AI will improve expense ratios at the top 50 insurers by two percentage points in 2026

- BCG estimates AI can reduce operating costs per premium dollar by 15–25%, translating to $35–60 billion in savings

- Insurance AI leaders generated 6.1x the total shareholder return of AI laggards over five years — well above the 2–3x multiple seen in most sectors

Employee Empowerment

Human agents, adjusters, and underwriters shift away from repetitive, data-heavy tasks toward complex decisions, relationship management, and cases requiring empathy or nuanced judgment. Agentic AI also creates new roles in AI oversight, data governance, and model monitoring.

The displacement concern is overstated. Only 5% of insurance sales agent tasks are estimated to be fully automated; 48% are expected to be augmented. The dominant model is human-AI collaboration.

That collaboration only works if agents are genuinely ready for higher-complexity work. Knowmax's Learning Management System supports this directly — structured learning paths combining courses, interactive lessons, and assessments reduce time to proficiency by up to 40%, so agents can handle the interactions AI escalates to them confidently.

Key Challenges and Considerations for Agentic AI Adoption

Data and Infrastructure Readiness

Agentic AI is only as effective as the data it draws from. Fragmented legacy systems, siloed databases, and unstructured documents require foundational data governance and integration work before deployment. Starting with a clean, unified data model is a prerequisite, not a parallel workstream.

Key data readiness statistics for insurers:

- 81% of AI professionals report significant data quality issues at their organisations

- 85% say leadership is not adequately addressing those issues

- Only 4% of insurers are currently reskilling their workforce at the required scale

Governance and Ethics

When an AI agent makes a coverage denial or payout decision, accountability must be clearly defined. Insurers need explainability frameworks, bias auditing protocols, and human-in-the-loop escalation paths that satisfy both internal risk standards and external regulatory expectations.

The regulatory landscape is already setting hard requirements:

- NAIC Model Bulletin (adopted December 4, 2023) — establishes insurer accountability standards for AI use

- EU AI Act — classifies life and health insurance pricing as high-risk AI

- Colorado SB21-169 — prohibits unfair discrimination using external consumer data and AI, requiring corrective action for consumer harms

Compliance architecture must be built into systems from the start — retrofitting governance after deployment consistently fails audits and increases remediation costs.

Change Management and Talent

Organisational adoption — not technology — is the most common barrier to getting ROI from agentic AI. Insurers must invest in upskilling staff, redefine roles around AI collaboration, and build cultural acceptance through clear communication and phased rollouts.

The talent picture reinforces how urgent this is:

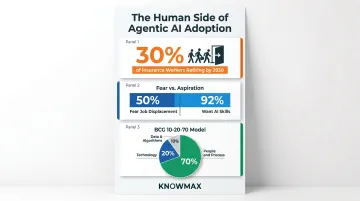

- 30% of insurance workers will reach retirement age by 2030, deepening the skills gap

- 50% fear job displacement from AI — yet 92% want to acquire generative AI skills

- BCG's 10-20-70 model puts 70% of AI-first transformation effort in people and process — only 10% in algorithms, 20% in technology and data

Gartner predicts 40% of agentic AI projects will be cancelled by 2027 — driven by escalating costs, unclear business value, and risk control gaps. That figure is better than the 70–85% historical failure rate for enterprise tech, but it still signals that execution discipline, not the technology itself, will determine which insurers succeed.

Frequently Asked Questions

What is the difference between agentic AI and traditional AI in insurance?

Traditional AI identifies patterns or flags anomalies but requires humans to act; agentic AI autonomously executes complete workflows—from intake to resolution—looping in human oversight only for exceptions. It owns end-to-end processes rather than assisting with individual steps.

What are the most impactful use cases of agentic AI in insurance?

Claims processing, underwriting automation, fraud detection, and customer service/policy servicing deliver the highest impact. These gains compound when use cases are connected rather than siloed — each integrated workflow reduces friction in the next.

How does agentic AI improve the claims process?

Automated FNOL, AI-driven damage assessment, intelligent routing, and faster end-to-end closure for straightforward claims reduce cycle times from weeks to days or hours. Complex cases receive focused human attention with full context already assembled, improving both speed and quality.

What challenges should insurers prepare for when adopting agentic AI?

The three main barriers are data readiness (clean, unified data models), AI governance and regulatory compliance (explainability, bias testing, audit trails), and organizational change management (upskilling, role redefinition, cultural acceptance). Most failed deployments trace back to these foundations — not the technology itself.

Will agentic AI replace insurance agents and adjusters?

The evidence points to augmentation, not replacement: 5% of insurance sales agent tasks are estimated to be fully automated, while 48% are expected to be augmented. Agentic AI handles repetitive, data-intensive tasks while humans focus on complex cases, relationship management, and decisions requiring empathy and judgment.

How do insurers maintain regulatory compliance when using agentic AI?

Compliance requires explainability frameworks, audit trails, bias testing, and adherence to standards like NAIC, HIPAA, and GDPR. Platforms should hold certifications (SOC 2, ISO 27001) before deployment — compliance built into system architecture from the start, not patched in after the fact.