Traditional underwriting processes create compounding delays: intake waits on data gathering, verification waits on intake, scoring waits on verification. Each manual handoff adds time, and straightforward applications get trapped behind complex cases in the same queue.

AI agents eliminate these bottlenecks by autonomously orchestrating the entire underwriting chain — pulling data from multiple sources, parsing unstructured documents via NLP, scoring risk in real time, and managing applicant follow-up without human intervention. This article examines the revenue cost of underwriting delays, how AI agents differ categorically from older RPA tools, sector-specific applications in banking versus insurance, and what responsible deployment requires in regulated industries.

TLDR

- Manual underwriting steps (intake, verification, scoring, routing) compound sequentially, turning single-day lags into week-long backlogs

- AI agents differ from RPA by reasoning across multi-step goals, processing unstructured documents, and adapting to exceptions autonomously

- AI agents run data prefill, document analysis, risk scoring, and applicant communication in parallel — not sequentially

- Human underwriters shift to complex judgment cases, focusing expertise where it matters most

Why Underwriting Delays Cost More Than You Think

Underwriting is a chain of dependent tasks where delay at each stage compounds total wait time. Intake waits on data gathering, verification waits on intake, risk scoring waits on verification, and routing waits on scoring. A one-day lag at each step turns simple applications into week-long queues where straightforward cases get trapped behind complex ones.

The financial impact is measurable. Freddie Mac's 2024 Cost to Originate Study found that lenders with high technology usage close loans in approximately 34 days versus 39 days for low-usage lenders — a 5-day gap that directly impacts application completion rates. Average origination costs have increased 35% over the past three years, reaching approximately $11,600 per loan industry-wide.

When underwriting stretches into weeks, applicants simply choose faster competitors. LIMRA's 2025 Insurance Barometer Study found that 52% of consumers say they are somewhat or very likely to buy a policy issued using accelerated underwriting. Speed has become a direct competitive differentiator.

The "administrative tax" on underwriters is substantial. McKinsey research shows that 30-40% of underwriting time is spent on administrative tasks such as re-keying data and chasing documents rather than actual risk analysis. Skilled professionals end up doing clerical work that AI agents can handle in seconds.

Delays also drive premium leakage — a cost that rarely gets a line item but consistently hits loss ratios. When underwriting takes too long, an applicant's risk profile can shift between application and final decision, producing pricing inaccuracies that erode margins. Verisk identifies three recurring culprits:

- Inaccurate property data that hasn't been refreshed at the point of decision

- Outdated valuations that no longer reflect current market or replacement costs

- Delayed risk assessment that lets exposure shift before a policy is bound

These issues are especially acute in fast-moving lines like commercial property and health insurance, where conditions change quickly.

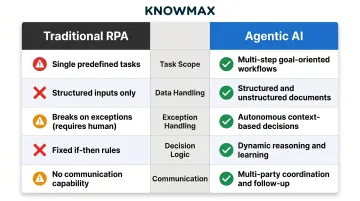

AI Agents vs. Basic Automation: What's Actually Different

Rule-based RPA handles predictable, structured tasks well but breaks when documents arrive in unstructured formats, data is incomplete, or exceptions require contextual judgment — which describes most real-world loan or insurance applications. RPA scripts follow a fixed sequence and require human intervention when anything deviates.

AI agents are goal-oriented systems that decompose multi-step objectives, decide which tools or data sources to use at each step, handle exceptions autonomously, and communicate with multiple external parties. Rather than executing a predefined script, agents reason through workflows and adapt to the context they encounter.

Key Differences: RPA vs. Agentic AI

| Dimension | Traditional RPA | Agentic AI |

|---|---|---|

| Task Scope | Single, predefined tasks | Multi-step, goal-oriented workflows |

| Data Handling | Structured inputs only | Structured + unstructured documents |

| Exception Handling | Breaks; requires human intervention | Autonomous context-based decisions |

| Decision Logic | Fixed if-then rules | Dynamic reasoning and learning |

| Communication | None (passes data only) | Multi-party coordination and follow-up |

McKinsey's 2025 analysis describes a future where nearly all customer onboarding functions are delivered through AI multi-agent systems acting as virtual coworkers. For insurance underwriting specifically, McKinsey identifies six specialized agent roles:

- Intake Agent

- Risk Profiling Agent

- Pricing and Product Agent

- Compliance and Fairness Agent

- Decision Orchestrator Agent

- Learning and Feedback Agent

A North American insurer is already using agentic processes to codify the implicit judgments underwriters have historically made by instinct.

Gartner predicts that 33% of enterprise software applications will include agentic AI by 2028 — up from less than 1% in 2024 — and that at least 15% of day-to-day work decisions will be made autonomously by that same year.

The same report carries a pointed warning: over 40% of agentic AI projects will be canceled by end of 2027 due to escalating costs, unclear business value, or inadequate risk controls. Deployments that succeed tend to target specific, well-defined workflows with measurable outcomes from the start.

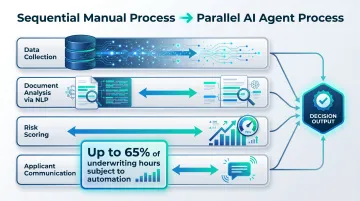

That's where architecture matters. The multi-agent model emerging in financial services deploys specialized agents working in parallel rather than sequentially. Instead of one process waiting for another to complete, multiple agents run simultaneously and synchronize only when necessary — eliminating the cascading delays that plague traditional sequential workflows.

How AI Agents Eliminate Underwriting Bottlenecks Step by Step

Automated Data Collection and Document Processing

AI agents pull applicant data autonomously from credit bureaus, public property records, claims histories, medical information bureaus, and third-party risk databases — eliminating the back-and-forth between underwriters, agents, and applicants that typically adds days to intake.

MIB Group's EHR Service returns electronic health records 90% faster than traditional Attending Physician Statements (APS), with more than 75% of records delivered within 24 hours and almost 20% within the first five minutes of searching. Average cost savings reach 50% per record, pointing to digital data retrieval as the biggest single efficiency gain in life insurance underwriting.

LIMRA research from 2022 found that 83% of insurers with accelerated underwriting programmes use prescription drug databases with a 90% median hit rate. Over one-third of companies with accelerated underwriting have a fully electronic process requiring no human touch, and one in five insurers have stopped collecting blood samples entirely.

NLP-powered document processing replaces manual review by reading and extracting key data from medical records, loss run reports, financial statements, and engineering surveys in seconds rather than hours. This turns unstructured content into structured risk inputs without a human reviewer touching each document.

Accenture's 2025 survey of 430 senior underwriting executives found that up to 65% of working hours in underwriting are subject to automation or augmentation. Intelligent email pre-sorting adoption is expected to grow from 10% to 75%, and intelligent ingestion (data extraction from submissions) from 9% to 68%, within three years.

Real-Time Risk Scoring and Intelligent Triage

Instead of a one-time score calculated at manual review, AI agents produce risk scores that update continuously as new data arrives. This dynamic scoring improves pricing accuracy and supports better loss ratio outcomes.

Munich Re, citing McKinsey data, reports that AI has delivered measurable impact including a 10%-20% improvement in new-agent success rates and a 10%-15% increase in premium growth. McKinsey's 2025 analysis identifies a 20% to 40% reduction in costs to onboard new customers and a potential double-digit bottom-line lift from transforming an entire domain such as underwriting.

Intelligent triage and escalation routing allows AI agents to auto-approve straightforward low-risk applications immediately and route only genuinely complex cases to human underwriters. LIMRA found that over one-third of companies with an accelerated underwriting programme have a fully electronic straight-through process requiring no human intervention, and 60% of companies plan to implement such a process in the future.

This intelligent routing does not sacrifice approval rates — it increases underwriting accuracy by ensuring that senior underwriters focus their expertise where institutional knowledge and complex judgment are genuinely required.

Multi-Party Communication and Knowledge Access

AI agents manage the full coordination loop autonomously, operating 24/7 and eliminating wait times tied to business hours. Across a typical underwriting workflow, they handle:

- Sending follow-up requests to applicants for missing documents

- Coordinating with medical providers or property inspectors

- Pushing status updates to brokers across channels

- Logging every interaction for audit and compliance purposes

However, AI agents are only as effective as the knowledge and decision logic they can access. Underwriting rules, compliance scripts, and escalation procedures must be structured and accessible in real time — otherwise agents act on outdated or incomplete information.

This is where an AI-powered knowledge management platform like Knowmax serves as the structured decision intelligence layer. Knowmax's interactive decision trees convert complex underwriting SOPs into no-code guided workflows, enabling both AI agents and human reviewers to navigate conditional rules and escalation paths without ambiguity. Key platform capabilities relevant to underwriting include:

- CRM integration: fetches customer data dynamically at the point of decision

- Auto-traverse: navigates decision trees automatically based on incoming inputs

- Version control and audit trails: maintains a complete record for compliance in regulated environments

- Centralised knowledge: consolidates policy data, underwriting guidelines, and regulatory updates into one accessible layer

Banking vs. Insurance: Where AI Agents Have the Biggest Impact

Banking and Mortgage Lending

AI agents in loan underwriting automate income verification, credit analysis, debt-to-income calculations, and property valuation data retrieval.

Freddie Mac's 2024 Cost to Originate Study quantifies the impact across several automation tools:

- Loan Product Advisor (LPA): High-usage lenders originate loans for $1,500 (14%) less than low-usage lenders

- Automated Collateral Evaluation (ACE): Saves 7.3 days in cycle time per loan

- Asset and Income Modeler (AIM): Saves an additional 1.2 days per loan

- Full digital processing: Eliminates 2.2–12.3 hours of production time per loan; executives estimate up to 40% cost reduction

Fannie Mae's Day 1 Certainty program shows similarly concrete results across participating lenders:

- Taylor Morrison Home Funding: Cut application-to-approval time by 5 business days

- The Mortgage Firm: Reduced application-to-close time by as much as 11.9 days

- First Citizens Bank: Improved cycle times and borrower satisfaction within 60 days of implementation

Property & Casualty Insurance

Virtual property surveys using satellite imagery and computer vision remove the scheduling delay of physical inspections. Cape Analytics uses aerial and satellite imagery with AI to assess property conditions for underwriting, covering over 110 million structures across the United States. Named carrier partners include The Hartford for homeowners' insurance underwriting, Kin Insurance for instant quoting using roof condition data, and State Farm for roof condition rating in renewal underwriting.

ZestyAI's Z-FIRE model partners with Farmers Insurance and Berkshire Hathaway Guard for wildfire risk assessment using satellite imagery and AI, reporting its model is 10x more predictive of wildfire loss than legacy models based solely on fuel and slope.

Life & Health Insurance

AI agents communicate with medical providers, parse electronic health records through NLP, and compile findings into structured risk profiles. LIMRA found that over 80% of insurers met their goal of reducing the time it takes to issue a policy through accelerated underwriting programs. John Hancock reduced processing from weeks to minutes; Symetra achieved application to policy issuance in as little as 25 minutes.

The conversion advantage is measurable: when applicants receive decisions in days rather than weeks, acceptance rates improve meaningfully. LIMRA's 2025 Insurance Barometer Study confirms that 52% of consumers are somewhat or very likely to buy a policy issued using accelerated underwriting.

Keeping AI Agents Accountable: Compliance, Bias, and Human Oversight

Models trained on historical data can perpetuate discriminatory patterns if not actively audited. Responsible deployment requires regular algorithmic audits, diverse training data, and transparent decision rationale.

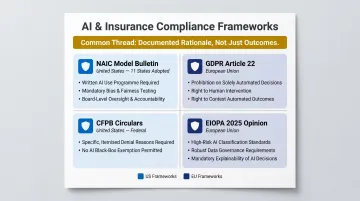

Four regulatory frameworks currently shape how AI-driven underwriting decisions must be governed:

| Regulation | Jurisdiction | Key Requirement |

|---|---|---|

| NAIC Model Bulletin on AI Systems (Dec 2023) | US — 11 states adopted as of April 2024 | Written AI System Programme covering governance, board oversight, risk controls, vendor oversight, and bias testing; documentation available to state regulators on request |

| GDPR Article 22 | EU | Right not to be subject to solely automated decisions with legal or significant effects; controllers must provide human intervention, the ability to express a view, and the right to contest |

| CFPB Circulars 2022-03 & 2023-03 | US | Lenders using complex algorithms must still provide specific, accurate reasons for credit denials under ECOA and Regulation B — no AI exemption |

| EIOPA 2025 Opinion on AI Governance | EU | AI used in life and health insurance risk assessment classified as high-risk under the EU AI Act; requires robust data governance to minimize bias, explainability, and human oversight |

These frameworks share a common thread: regulators expect documented rationale, not just outcomes. That's where the architecture of compliant AI matters.

Properly configured AI agents maintain a full audit trail of every data point accessed and every decision step taken, making compliance reviews faster rather than a separate manual process. Platforms like Knowmax — which holds SOC 2, ISO 27001, GDPR, and HIPAA certifications — support this by providing audit-ready knowledge governance, ensuring the content and decision logic surfaced to underwriting agents is traceable and securely managed in regulated environments.

The human-in-the-loop model means AI agents handle volume and routine decisions while senior underwriters focus on cases requiring institutional knowledge and complex judgment. This role shift increases rather than reduces underwriting accuracy by ensuring expert attention is applied where it delivers the most value.

Frequently Asked Questions

How do AI agents reduce underwriting delays in banking and insurance?

AI agents eliminate delays by automating data collection, document review, risk scoring, and applicant follow-up simultaneously, rather than waiting for each step to finish before starting the next.

What is the difference between AI agents and traditional RPA in underwriting?

RPA handles single, structured, predefined tasks and fails when inputs change. AI agents are goal-oriented systems that process unstructured documents, handle exceptions on their own, and coordinate multi-step workflows without constant human intervention.

What underwriting tasks can be fully automated versus which still need human review?

Routine, data-complete applications meeting clear eligibility criteria can be auto-approved, while complex cases, high-value policies, and edge cases with ambiguous risk signals are routed to human underwriters. The split varies by insurer and loan type.

How do AI agents handle compliance requirements during underwriting?

AI agents can be configured to enforce compliance rules in real time, check every decision against relevant regulations, and maintain a complete audit trail of every data point and decision step This reduces compliance risk, provided the system is properly governed and regularly audited.

What are the risks of using AI agents in underwriting decisions?

Primary risks include algorithmic bias from historical training data, opaque decision logic that is difficult to explain to regulators or applicants, and over-reliance on automation for cases requiring human judgment. Each risk can be addressed through model audits, explainability tools, and clear escalation rules that keep humans accountable for high-stakes decisions.

How does AI-assisted underwriting affect the customer experience?

Faster decisions reduce application abandonment. Applicants who hear back in days rather than weeks are measurably more likely to accept an offer. Around-the-clock autonomous follow-up also keeps applicants informed without business-hours wait times.