Introduction

Insurance companies face mounting pressure from every direction. Customers expect instant claims resolution—82% demand payouts within five days—while regulators demand precision and operational costs continue climbing. Yet the average auto claim still takes 19.3 days to resolve, and property claims now exceed 32 days from filing to completion.

That gap between expectation and reality has a real cost: 83% of US consumers would switch carriers after a poor claims experience. The operational side isn't holding up either — claims adjusters spend more than 70% of their time on manual administrative work rather than complex judgment calls. When catastrophe events strike, volumes can spike 3–10x within days, overwhelming those workflows at the exact moment policyholders need support most.

Agentic AI addresses this directly. Unlike rule-based automation, agentic AI systems plan, execute, and adapt multi-step workflows autonomously — handling the coordination work that currently consumes adjuster time. This article examines how insurers are deploying these systems to compress claims cycles and improve customer experience from first notice of loss to final settlement.

TLDR

- Agentic AI executes end-to-end insurance workflows—intake to settlement—without step-by-step human direction, going well beyond chatbots or generative AI

- In claims, it cuts cycle times from days to hours via automated FNOL, damage assessment, fraud detection, and straight-through processing

- For CX, it powers 24/7 virtual agents, proactive policyholder outreach, and real-time agent-assist tools that reduce handling time and errors

- Adoption jumped from 8% to 34% year-over-year—early movers like Allianz are already settling claims in hours, not days

What Is Agentic AI in Insurance?

Agentic AI refers to autonomous, goal-driven systems that independently perceive data inputs, plan actions, execute tasks, and refine behavior through feedback loops—no step-by-step human direction required.

McKinsey defines it as software "that has the agency to act on behalf of a user or system to perform tasks," distinguishing it from chatbots by its ability to "plan, collaborate, and complete tasks" rather than merely answer queries.

How It Differs from Traditional Automation

Traditional rule-based AI flags issues but stops there—it might identify a suspicious claim but requires human action to proceed. Generative AI creates content but needs human direction to execute next steps. Agentic AI acts: it can escalate a claim, trigger an investigation workflow, notify the adjuster, and update the claimant—all autonomously and in sequence.

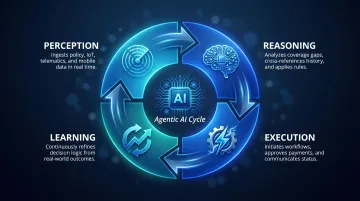

Gartner warns of "agent washing," where vendors rebrand existing RPA and chatbot products as "agentic" without adding real autonomous capabilities. True agentic AI operates through a continuous cycle:

- Perception: Ingests data from policy systems, IoT sensors, telematics, mobile uploads

- Reasoning: Analyzes coverage, cross-references claim history, applies business rules

- Execution: Initiates workflows, approves payments, schedules adjusters, communicates status

- Learning: Refines decision logic based on outcomes and feedback

Regulatory Guardrails for Insurance

In a heavily regulated industry, agentic AI operates within predefined compliance and business logic boundaries. Human oversight kicks in for high-stakes decisions: disputed liability, large settlements, or claims that exceed automated authority thresholds.

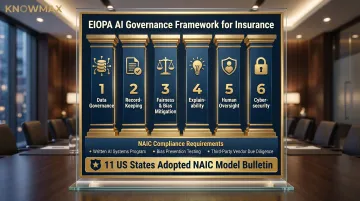

This structure maintains audit trails, explainability, and adherence to frameworks like the NAIC Model Bulletin and EIOPA's AI Governance Opinion.

That's the practical gap between a chatbot and an agentic system. A chatbot answers a coverage question. An agentic AI reviews the policy, identifies a gap, recommends a rider, and initiates the update—in a single, uninterrupted workflow.

Why Legacy Insurance Operations Are Falling Short

Manual processes drain productivity and revenue. McKinsey research shows underwriters spend 30-40% of their time on administrative tasks; claims adjusters spend more than 70% on non-core manual work like data re-keying and document verification.

The Revenue Risk of Poor Experience

Poor claims experiences put billions in premium revenue at risk:

- 83% of consumers would switch carriers after a poor claims experience

- 60% would switch for more personalized service alone, even without claims disputes or pricing issues

- Only 4% are at risk of attrition when digital claims experience is rated "excellent"

These switching risks compound an existing problem: cycle times. Auto claims average 19.3 days for repairable vehicles; property claims now exceed 32 days.

When catastrophe events strike, volumes spike 3-10x within days — creating bottlenecks that leave policyholders waiting at their most vulnerable moments.

Traditional automation handles linear tasks well but struggles when workflows get complex — filing FNOL, verifying coverage across multiple policies, coordinating third-party inspections, detecting fraud signals, and routing adjuster assignments. Agentic AI addresses this directly: systems that execute these end-to-end workflows autonomously, adapting in real time when exceptions arise.

Agentic AI Use Cases: Accelerating Claims Processing

Automated FNOL and Intake

First Notice of Loss (FNOL) represents the critical first touchpoint in the claims journey. Agentic AI transforms it from a manual intake queue into an automated workflow that begins the moment a policyholder submits a claim through mobile apps, IoT sensors, telematics data, or web portals.

How it works:

- Automatically ingests claim details, photos, and supporting documents

- Triggers claim creation in core systems without human intervention

- Verifies coverage eligibility by cross-referencing policy terms in real time

- Initiates initial triage based on claim type, severity, and complexity

- Assigns priority and routes to appropriate workflows or adjusters

Allianz launched its first agentic AI solution to automate food spoilage claims, cutting processing times from days to hours. The system handles FNOL intake and claims adjudication end-to-end for this high-volume, standardized claim type.

Automated document verification runs in parallel: AI agents validate uploaded photos, invoices, and medical records, match them against policy terms, and confirm coverage eligibility — compressing a multi-day review into near-real-time processing.

McKinsey estimates automation in FNOL can reduce processing time by up to 50%.

Damage Assessment and Straight-Through Settlement

Computer vision enables AI agents to analyze images or video of damaged property, vehicles, or assets uploaded by policyholders or captured by drones. This allows automated damage quantification without requiring an adjuster site visit for routine claims.

The straight-through processing advantage:

The capability is clear — but industry adoption tells a different story. Fewer than 10% of claims are processed straight-through across all lines of business, and nearly 60% of insurers have no STP capability in claims. This contrasts sharply with underwriting, where more than 80% of personal lines insurers already use automated processing.

Once coverage is validated and damage assessed within defined thresholds, the AI agent can approve and trigger payment automatically. Early adopters report 70–80% reductions in processing time for routine claims, with low-complexity claims approved in hours instead of weeks.

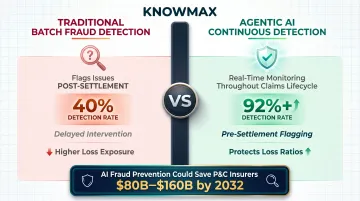

Continuous Fraud Detection

Unlike batch-processing fraud models that flag issues after settlement, agentic AI runs continuous fraud pattern analysis throughout the claims lifecycle. It cross-references claim details, historical data, and behavioural signals in real time — detecting anomalies like:

- Inconsistent damage patterns vs. incident description

- Duplicate claims across multiple policies or carriers

- Suspicious timing or location data from telematics

- Fraudulent document uploads identified through computer vision

One implementation using computer vision for damage detection detected over 92% of fraudulent images compared to a 40% detection rate with manual review — cutting operational costs per claim by more than half.

Deloitte estimates AI-driven fraud prevention could save P&C insurers $80 billion to $160 billion by 2032.

The key advantage: agentic AI can flag or pause suspicious claims before settlement, not after, protecting loss ratios while maintaining fast processing for legitimate claims.

How Agentic AI Elevates Insurance Customer Experience

AI-Powered Self-Service and Proactive Engagement

Today's virtual agents go far beyond FAQ chatbots. Agentic AI systems handle end-to-end complex service requests—policy updates, claims follow-ups, coverage inquiries, beneficiary changes—across voice, chat, email, and app channels simultaneously, 24/7.

A concrete example: A homeowner asks about flood coverage through a mobile app chat. The agentic AI system reviews the current policy, identifies that flood coverage isn't included, calculates the premium for a recommended rider based on the property's location and flood zone, and initiates the policy update—all in a single interaction, with the policyholder simply approving the change.

That kind of seamless interaction is just one side of the picture. Agentic AI also shifts the insurer-policyholder relationship from reactive to protective by monitoring external signals—weather events, life changes, renewal dates—and proactively reaching out with personalised alerts and risk mitigation advice.

Research analyzing 380,000+ claims text messages found that proactive outbound communication made inbound policyholder questions three times less likely. Claims with at least one proactive message had only a 19% inbound question rate versus 60% for claims without proactive outreach.

Weather-based alerts deliver measurable value: 90% of policyholders find value in receiving weather alerts from their insurer, with average savings of $3,000 per hail claim when preventative action is taken after a proactive alert.

Personalised Engagement and Agent Empowerment

Agentic AI enables targeted policy recommendations triggered by life event signals. A new vehicle purchase, marriage, home acquisition, or health data change can prompt the AI to suggest relevant coverage upgrades—improving cross-sell conversion and policyholder satisfaction simultaneously.

Agent-assist for complex claims:

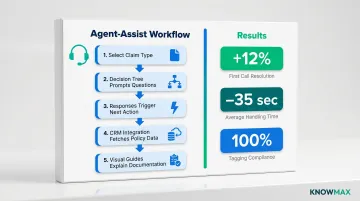

Even in human-handled claims calls, agentic AI serves as a real-time co-pilot. Insurance contact centre agents handling complex multi-policy or multi-party claims must navigate intricate coverage rules under pressure—with little room for error.

Knowledge management platforms like Knowmax address this directly through guided resolution workflows and interactive decision trees. During a live property damage claim call, for example:

- The agent selects the claim type from predefined categories

- The decision tree prompts specific questions about incident date, damage extent, and documentation

- Each response triggers the next relevant question or action step

- The system integrates with CRM data to fetch policy details and claim history

- Visual guides and file attachments help explain complex documentation requirements

Every agent follows the same structured path, which eliminates guesswork and keeps responses consistent across tenure levels and product lines. In one fintech deployment, guided workflows produced a 12% increase in First Call Resolution (FCR), a 35-second reduction in Average Handling Time (AHT), and 100% tagging compliance.

These tools are particularly impactful for insurance contact centres where agents must balance speed with regulatory compliance and accuracy across multiple jurisdictions and product lines.

Post-claim retention is another area where automation pays off. Agentic AI automatically triggers satisfaction surveys, re-engagement messages, or loyalty offers after claim resolution—converting a high-stress touchpoint into a retention opportunity.

The stakes are significant: only 4% of customers are at risk of attrition when their digital claims experience is rated excellent. Automated follow-up directly moves that needle on renewal rates.

Preparing Your Insurance Operations for Agentic AI

Data Readiness: The Non-Negotiable Foundation

AI agents require clean, unified data across policy administration, claims, and customer systems. Siloed or inconsistent data degrades agent performance and creates compliance risks.

Action steps:

- Audit data quality across all source systems

- Build a unified data model that connects policy, claims, and customer records

- Establish data governance standards for accuracy, completeness, and timeliness

- Address legacy system integration gaps before scaling agentic AI initiatives

Insurers who skip this step often find their agents producing confident-sounding but factually wrong outputs — a costly problem when coverage decisions are on the line.

Governance and Compliance Requirements

Define what decisions agents can make autonomously versus what requires human escalation. For insurance, this means:

- Documenting AI decision logic with clear business rules and thresholds

- Maintaining audit trails for all automated decisions and actions

- Ensuring compliance with GDPR, HIPAA, NAIC Model Bulletin requirements, and EIOPA's six-pillar framework (data governance, record-keeping, fairness/bias mitigation, explainability, human oversight, cybersecurity)

- Implementing board-level oversight of AI governance programs

As of April 2024, 11 US states had adopted the NAIC Model Bulletin on AI use by insurers. Requirements include written AI Systems Program policies, bias prevention testing, and third-party vendor due diligence. Cross-functional AI governance boards are now standard among leading carriers.

Pilot-First Approach

Identify one high-impact, lower-risk use case to demonstrate ROI before expanding:

Good pilot candidates:

- Automating FNOL intake for a specific line of business

- Straight-through processing for low-complexity claims under a defined threshold

- Outbound renewal reminders and policy review scheduling

- Automated damage assessment for routine property claims

Establish clear success KPIs:

- Claims cycle time reduction (target: 30-50% for pilot segment)

- Customer satisfaction scores (CSAT)

- Average handling time (AHT)

- First call resolution (FCR) rates

- Straight-through processing percentage

A successful pilot gives leadership the evidence to fund broader rollout — and surfaces integration problems at a scale where they're still fixable.

Frequently Asked Questions

What is agentic AI in P&C insurance?

Agentic AI refers to autonomous, goal-oriented systems that execute complete workflows in property and casualty insurance—from claims intake to settlement—independently, within defined compliance guardrails, and without step-by-step human direction. Unlike traditional automation that flags issues, agentic AI plans, executes, and adapts multi-step processes.

What is an example of agentic AI in insurance?

A policyholder submits photos of vehicle damage via mobile app. The agentic AI system verifies coverage, assesses damage using computer vision, cross-checks for fraud signals, calculates repair costs, and issues a payout—all within hours and without manual adjuster involvement. The entire workflow executes autonomously from first notice to settlement.

What are the main applications of agentic AI?

Primary insurance applications span the full policy lifecycle:

- Automated claims processing (FNOL, damage assessment, settlement)

- Continuous fraud detection and investigation workflows

- Underwriting support and risk scoring

- 24/7 omnichannel customer service

- Proactive policyholder engagement (weather alerts, coverage gap notifications)

- Personalized product recommendations triggered by life events

How does agentic AI improve customer experience in insurance?

Agentic AI compresses claim resolution from days to hours and delivers always-on service across voice, chat, and mobile. Proactive risk communication reduces inbound questions by 3x, while real-time guided assistance helps human agents resolve complex cases faster.

What is the difference between agentic AI and traditional AI in insurance?

Traditional AI analyzes and flags—it identifies a suspicious claim but stops there. Agentic AI acts: it can escalate the claim, trigger an investigation workflow, notify the adjuster, and update the claimant, all autonomously and in sequence. The shift is from insight generation to autonomous execution.

What challenges should insurers expect when implementing agentic AI?

Key barriers include fragmented or poor-quality data across policy and claims systems, the need for governance frameworks defining human oversight thresholds, upfront investment in integration infrastructure and API development, and change management to align internal teams with AI-augmented workflows. Gartner predicts over 40% of agentic AI projects will be cancelled by end of 2027 due to escalating costs or unclear business value.

Where Does This Leave Insurers?

Agentic AI is no longer experimental. Full AI adoption in insurance jumped from 8% to 34% year-over-year, and early movers are already seeing measurable gains: claims processed in hours instead of days, fraud detection accuracy above 90%, and retention risk dropping to single digits when digital experience is strong.

Insurers that pilot high-impact use cases now, with clean data, clear governance, and defined KPIs, will build a compounding advantage in both retention and operational efficiency. The window for low-risk experimentation is narrowing.